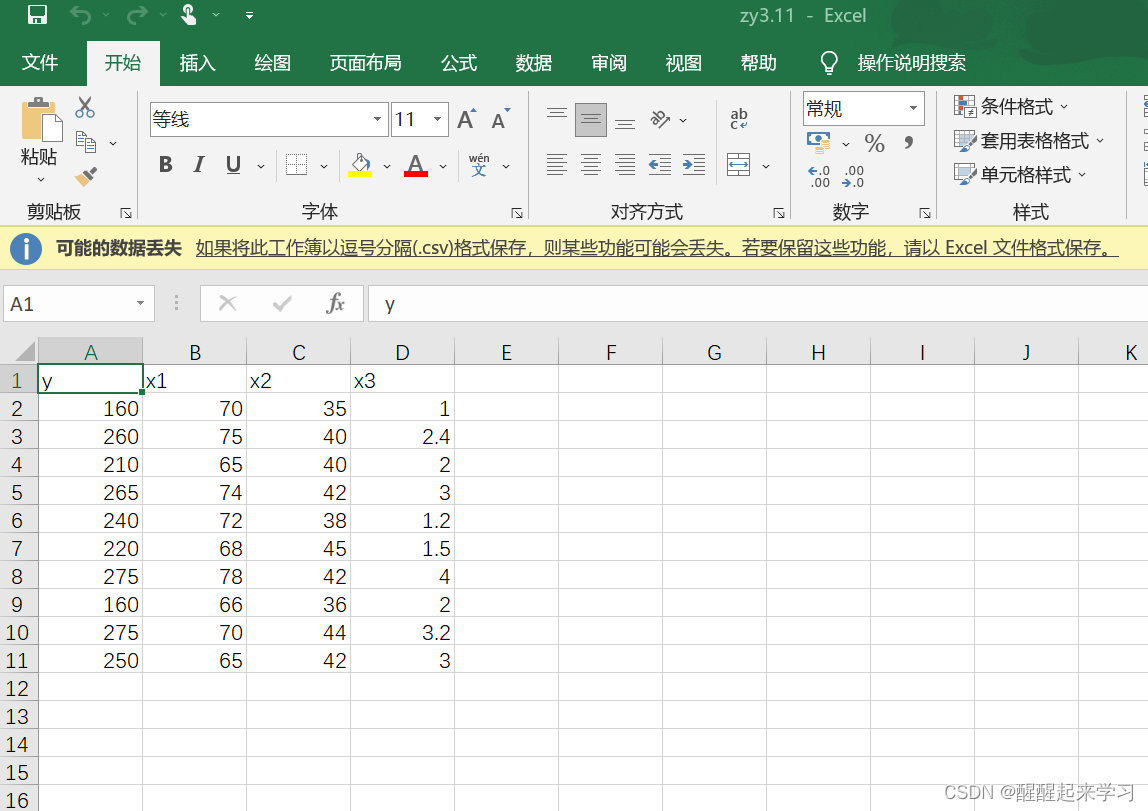

研究货运总量 y (万吨)与工业总产值 x1(亿元)、农业总产值 x2(亿元),居民非商品支出 X3 (亿元)的关系。数据见表3-9。

(1)计算出 y , x1 ,x2, x3 的相关系数矩阵。

(2)求 y 关于 x1 ,x2, x3 的三元线性回归方程。

(3)对所求得的方程做拟合优度检验。

(4)对回归方程做显著性检验。

(5)对每一个回归系数做显著性检验。

(6)如果有的回归系数没通过显著性检验,将其剔除,重新建立回归方程归方程的显著性检验和回归系数的显著性检验。

(7)求出每一个回归系数的置信水平为95%的置信区间

8)求标准化回归方程。

(9)求当X01=75,X02=42,X03=3.1时的,给定置信水平为95%,用算精确置信区间,手工计算近似预测区间

(10)结合回归方程对问题做一些基本分析

表3-9

注:每一小问的运行结果我以备注的形式 放在代码段里面

#导入需要的库和数据

import numpy as np

import statsmodels.api as sm

import statsmodels.formula.api as smf

from statsmodels.stats.api import anova_lm

import matplotlib.pyplot as plt

import pandas as pd

from patsy import dmatrices

# Load data

df = pd.read_csv('C:\\Users\\joyyiyi\\Desktop\\zy3.11.csv',encoding='gbk')

#解决第(!)问

#计算相关系数

cor_matrix = df.corr(method='pearson') # 使用皮尔逊系数计算列与列的相关性

# cor_matrix = df.corr(method='kendall')

# cor_matrix = df.corr(method='spearman')

print(cor_matrix)

'''

结果:

C:\Users\joyyiyi\AppData\Local\Programs\Python\Python39\python.exe C:/Users/joyyiyi/PycharmProjects/pythonProject6/0.py

y x1 x2 x3

y 1.000000 0.555653 0.730620 0.723535

x1 0.555653 1.000000 0.112951 0.398387

x2 0.730620 0.112951 1.000000 0.547474

x3 0.723535 0.398387 0.547474 1.000000

Process finished with exit code 0

'''#解决第(2)(3)(4)(5)问

result = smf.ols('y~x1+x2+x3',data=df).fit()

#print(result.params) #输出回归系数

print(result.summary())

print("\n")

print(result.pvalues) #输出p值

#

'''

运行结果:

C:\Users\joyyiyi\AppData\Local\Programs\Python\Python39\python.exe C:/Users/joyyiyi/PycharmProjects/pythonProject6/0.py

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.806

Model: OLS Adj. R-squared: 0.708

Method: Least Squares F-statistic: 8.283

Date: Wed, 09 Nov 2022 Prob (F-statistic): 0.0149

Time: 11:15:30 Log-Likelihood: -43.180

No. Observations: 10 AIC: 94.36

Df Residuals: 6 BIC: 95.57

Df Model: 3

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -348.2802 176.459 -1.974 0.096 -780.060 83.500

x1 3.7540 1.933 1.942 0.100 -0.977 8.485

x2 7.1007 2.880 2.465 0.049 0.053 14.149

x3 12.4475 10.569 1.178 0.284 -13.415 38.310

==============================================================================

Omnibus: 0.619 Durbin-Watson: 1.935

Prob(Omnibus): 0.734 Jarque-Bera (JB): 0.562

Skew: 0.216 Prob(JB): 0.755

Kurtosis: 1.922 Cond. No. 1.93e+03

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.93e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

Intercept 0.095855

x1 0.100197

x2 0.048769

x3 0.283510

dtype: float64

Process finished with exit code 0

'''

'''

(2)回答:线性方程:

Y=-348.2802+3.7540x1+7.1007x2+12.4475x3

(3)回答:R方=0.806,调整后R方=0.708

#或者说R=0.806>R0.05(8)=0.632,所以接受原假设,说明x与y有显著的线性关系

#或者说调整后的决定系数为0.708,说明回归方程对样本观测值的拟合程度较好。

(4)回答:做(F检验)

#原假设H0=β1=β2=β3=0

# F=8.283>F0.05(3,6)=4.76,或者说P=0.0149<α=0.05,说明拒绝原假设H0,x与y有显著的线性关系

(5)x1,x2,x3的t值分别为:

t1=1.942<t0.05(8)=1.943或者α=0.100>α=0.05,所以接受原假设,说明x1对y没有显著的影响

t2=2.465>t0.05(8)=1.943或者α=0.049<α=0.05,所以拒绝原假设,说明x1对y有显著的影响

t3=1.178<t0.05(8)=1.943或者α=0.284>α=0.05,所以接受原假设,说明x1对y没有显著的影响

'''

#在第(5)中发现除了x2外其他回归系数都未通过显著性检验,首先剔除x3看看效果

result = smf.ols('y~x1+x2',data=df).fit()

#print(result.params) #输出回归系数

print(result.summary())

print("\n")

print(result.pvalues) #输出p值

'''

运行结果:

C:\Users\joyyiyi\AppData\Local\Programs\Python\Python39\python.exe C:/Users/joyyiyi/PycharmProjects/pythonProject6/0.py

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.761

Model: OLS Adj. R-squared: 0.692

Method: Least Squares F-statistic: 11.12

Date: Wed, 09 Nov 2022 Prob (F-statistic): 0.00672

Time: 11:49:08 Log-Likelihood: -44.220

No. Observations: 10 AIC: 94.44

Df Residuals: 7 BIC: 95.35

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -459.6237 153.058 -3.003 0.020 -821.547 -97.700

x1 4.6756 1.816 2.575 0.037 0.381 8.970

x2 8.9710 2.468 3.634 0.008 3.134 14.808

==============================================================================

Omnibus: 1.265 Durbin-Watson: 1.895

Prob(Omnibus): 0.531 Jarque-Bera (JB): 0.631

Skew: -0.587 Prob(JB): 0.730

Kurtosis: 2.630 Cond. No. 1.63e+03

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.63e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

Intercept 0.019859

x1 0.036761

x2 0.008351

dtype: float64

Process finished with exit code 0

'''

#第(6)问回答:

在剔除x3后,回归方程Y=-459.6237+4.6756x1+8.9710x2

的拟合优度R2=0.761,F值=11.12(有所提高),回归系数的P值均小于0.05 因此回归系数均通过显著性t检验

#第(7)问回答:

通过summary()输出的回归结果最右边“[0.025 0.975]”这个位置可以看到

常数项,x1,x2的回归系数置信水平为95%的置信区间分别为:[-821.547,-97.700],[0.381,8.970],[3.134,14.808]

#标准化

dfnorm = (df-df.mean())/df.std()

new = pd.Series({'x1': 4000,'x2': 3300,'x3': 113000,'x4': 50.0,'x5': 1000.0})

newnorm = (new-df.mean())/df.std()

#标准化后构建无截距模型

resultnorm = smf.ols('y~x1+x2',data=dfnorm).fit()

print(resultnorm.summary())

'''

运行结果:

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.761

Model: OLS Adj. R-squared: 0.692

Method: Least Squares F-statistic: 11.12

Date: Fri, 11 Nov 2022 Prob (F-statistic): 0.00672

Time: 22:51:34 Log-Likelihood: -6.5156

No. Observations: 10 AIC: 19.03

Df Residuals: 7 BIC: 19.94

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -8.327e-17 0.175 -4.75e-16 1.000 -0.415 0.415

x1 0.4792 0.186 2.575 0.037 0.039 0.919

x2 0.6765 0.186 3.634 0.008 0.236 1.117

==============================================================================

Omnibus: 1.265 Durbin-Watson: 1.895

Prob(Omnibus): 0.531 Jarque-Bera (JB): 0.631

Skew: -0.587 Prob(JB): 0.730

Kurtosis: 2.630 Cond. No. 1.12

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Process finished with exit code 0

'''

第(8)问:

标准化后的回归方程为:

y=0.4792x1+0.6765x2-8.327e-17 # Load data

df = pd.read_csv('C:\\Users\\joyyiyi\\Desktop\\zy3.11.csv',encoding='gbk')

# print(df)

result = smf.ols('y~x1+x2',data=df).fit()

#标准化

dfnorm = (df-df.mean())/df.std()

new = pd.Series({'x1': 75,'x2': 42})

newnorm = (new-df.mean())/df.std()

#标准化后构建无截距模型

resultnorm = smf.ols('y~x1+x2',data=dfnorm).fit()

#单值预测

predictnorm = resultnorm.predict(pd.DataFrame({'x1': [newnorm['x1']],'x2': [newnorm['x2']]}))

#因为单值预测是基于标准化后的模型,需要对y值还原,y值还原方法:

ypredict = predictnorm*df.std()['y'] + df.mean()['y']

print("ypredict:")

print(ypredict)

#区间

predictions = result.get_prediction(pd.DataFrame({'x1': [75],'x2': [42]}))

print('置信水平为95%,区间预测:')

print(predictions.summary_frame(alpha=0.05))

#近似预测区间:

ylow=267.83-2*np.sqrt(result.scale)

yup=267.83+2*np.sqrt(result.scale)

print(ylow,yup)

'''

运行结果:

C:\Users\joyyiyi\AppData\Local\Programs\Python\Python39\python.exe C:/Users/joyyiyi/PycharmProjects/pythonProject6/回归作业.py

ypredict:

0 267.829001

dtype: float64

置信水平为95%,区间预测:

mean mean_se ... obs_ci_lower obs_ci_upper

0 267.829001 11.782559 ... 204.435509 331.222493

[1 rows x 6 columns]

219.66776823691464 315.99223176308533

Process finished with exit code 0

'''

第(9)问:

y0的预测值为267.829;

y0预测值的置信水平为95%的精确置信区间为:[204.44,331.22],

y0近似预测区间为:[219.67,315.99]

在做这次作业的时候因为不确定答案对不对,参考了csdn的另一位朋友的文章:

R语言之多元线性回归xt3.11_princess yang的博客-CSDN博客_为了研究货运量y与工业总产值x1

这篇写的很好,比我更有条理哦