Section B-TWO questions ONLY to be attempted

(a)Accounting for retirement benefits remains one of the most challenging areas in financial reporting. The values being reported are significant, and the estimation of these values is complex and subjective. Standard setters and preparers of financial statements find it difficult to achieve a measure of consensus on the appropriate way to deal with the assets and costs involved. SSAP24 Accounting for Pension Costs' focused on the profit and loss account, viewing retirement benefits as an operating expense. However, FRS17 Retirement Benefits' concentrates on the balance sheet and the evaluation of the pension fund. The philosophy and rationale of the two statements are fundamentally opposed. Required: (i)Describe four key issues in the determination of the method of accounting for retirement benefits in respect to of defined benefit plans; Discuss how FRS17 Retirement Benefits' deals with these key issues and to what extent it provides solutionsto the problems of accounting for retirement benefits.

B-2 部分仅可尝试的问题

(a) 退休福利会计仍然是财务报告中最具挑战性的领域之一。所报告的值非常重要,并且这些值的估计是复杂且主观的。标准制定者和财务报表编制者发现很难就处理所涉及资产和成本的适当方式达成一定程度的共识。 SSAP24 养老金成本会计重点关注损益账户,将退休福利视为运营费用。然而,FRS17 退休福利的重点是资产负债表和养老基金的估值。这两种说法的哲学和基本原理是根本对立的。

必需的:

(i)说明确定设定受益计划退休金核算方法时的四个关键问题;

讨论 FRS17 退休福利如何处理这些关键问题,以及它在多大程度上为退休福利会计问题提供了解决方案。

ChatGPT回答:

Accounting for retirement benefits, especially in the context of defined benefit plans, involves several key issues:

-

Measurement of the Obligation: The calculation of the pension obligation involves actuarial assumptions about demographic variables (like employee turnover and mortality) and financial variables (like future salary increases, the rate of return on plan assets, and discount rates for present valuing future obligations). These assumptions can have a significant impact on the size of the reported obligation.

-

Recognition and Timing of Expenses: Deciding when to recognize the costs associated with pension benefits can be complex. It involves determining the period over which the costs should be recognized, which could be during the employees’ working lives, at the time the pensions are paid, or some other period.

-

Valuation of Plan Assets: Defined benefit plans often involve investments intended to fund the future obligations. The measurement of these plan assets at fair value, which can fluctuate based on market conditions, adds to the complexity.

-

Presentation in Financial Statements: How pension costs and obligations are presented in financial statements, whether in the profit and loss account or on the balance sheet, affects the perceived financial position and performance of the entity.

扫描二维码关注公众号,回复: 17222055 查看本文章

FRS17 'Retirement Benefits' aims to address these issues as follows:

退休福利的会计处理,特别是在设定受益计划的背景下,涉及几个关键问题:

1.义务的计量:养老金义务的计算涉及人口变量(如员工流动率和死亡率)和财务变量(如未来工资增长、计划资产的回报率以及现值未来义务的贴现率)的精算假设。这些假设可能对报告义务的规模产生重大影响。

2.费用的确认和时间安排:决定何时确认与养老金福利相关的成本可能很复杂。它涉及确定应确认成本的期间,可以是在雇员的工作期间、支付养老金时或其他某个期间。

3.计划资产的估值:设定受益计划通常涉及旨在为未来义务提供资金的投资。这些计划资产的公允价值可能会根据市场状况而波动,这增加了复杂性。

4.财务报表中的列报:养老金成本和义务在财务报表中的列报方式,无论是在损益表中还是在资产负债表中,都会影响实体的财务状况和业绩。

FRS17“退休福利”旨在解决这些问题,具体如下:

-

It requires the pension scheme liabilities to be measured on an actuarial basis using the projected unit method, which anticipates future salary increases. This provides a more realistic measure of the company’s obligations.

-

The standard mandates that the expected costs of providing pensions to employees are recognized over the period that the company benefits from the employees' services, which aligns the expense recognition with the earning period of the benefits.

-

FRS17 also requires the assets of the pension fund to be measured at fair value, reflecting current market conditions. This fair value must be disclosed in the financial statements, which improves transparency.

-

The standard stipulates that full disclosure of the retirement benefit costs and obligations should be provided on the balance sheet, rather than just through the profit and loss account. This shift ensures that the financial statements more accurately reflect the company's financial status by recognizing all known liabilities and the resources set aside to meet them.

In essence, FRS17 provides a framework that aims to give a true and fair view of an entity's retirement benefit obligations and the resources available to meet them, making the financial statements more useful for users. However, the standard also introduces volatility into the financial statements due to the requirement to measure plan assets and liabilities at fair value, which can fluctuate over time.

它要求使用预计未来工资增长的预计单位法在精算基础上计量养老金计划负债。这为公司的义务提供了更现实的衡量标准。

该准则规定,向员工提供养老金的预期成本应在公司从员工服务中受益的期间内确认,从而使费用确认与福利的赚取期间保持一致。

FRS17 还要求养老基金的资产以公允价值计量,反映当前的市场状况。该公允价值必须在财务报表中披露,从而提高透明度。

该准则规定,应在资产负债表上全面披露退休福利成本和义务,而不仅仅是通过损益表。这一转变通过确认所有已知负债以及为满足这些负债而预留的资源,确保财务报表更准确地反映公司的财务状况。

从本质上讲,FRS17 提供了一个框架,旨在真实、公平地反映实体的退休福利义务以及可用于履行这些义务的资源,从而使财务报表对用户更有用。然而,由于要求以公允价值计量计划资产和负债,该准则也给财务报表带来了波动性,而公允价值可能会随着时间的推移而波动。

FRS 17 deals with the accounting treatment of defined contribution pension schemes and defined benefit pension schemes.

中文(简体)

FRS 17 涉及固定缴款养老金计划和固定福利养老金计划的会计处理。

根据图片的内容,原文如下:

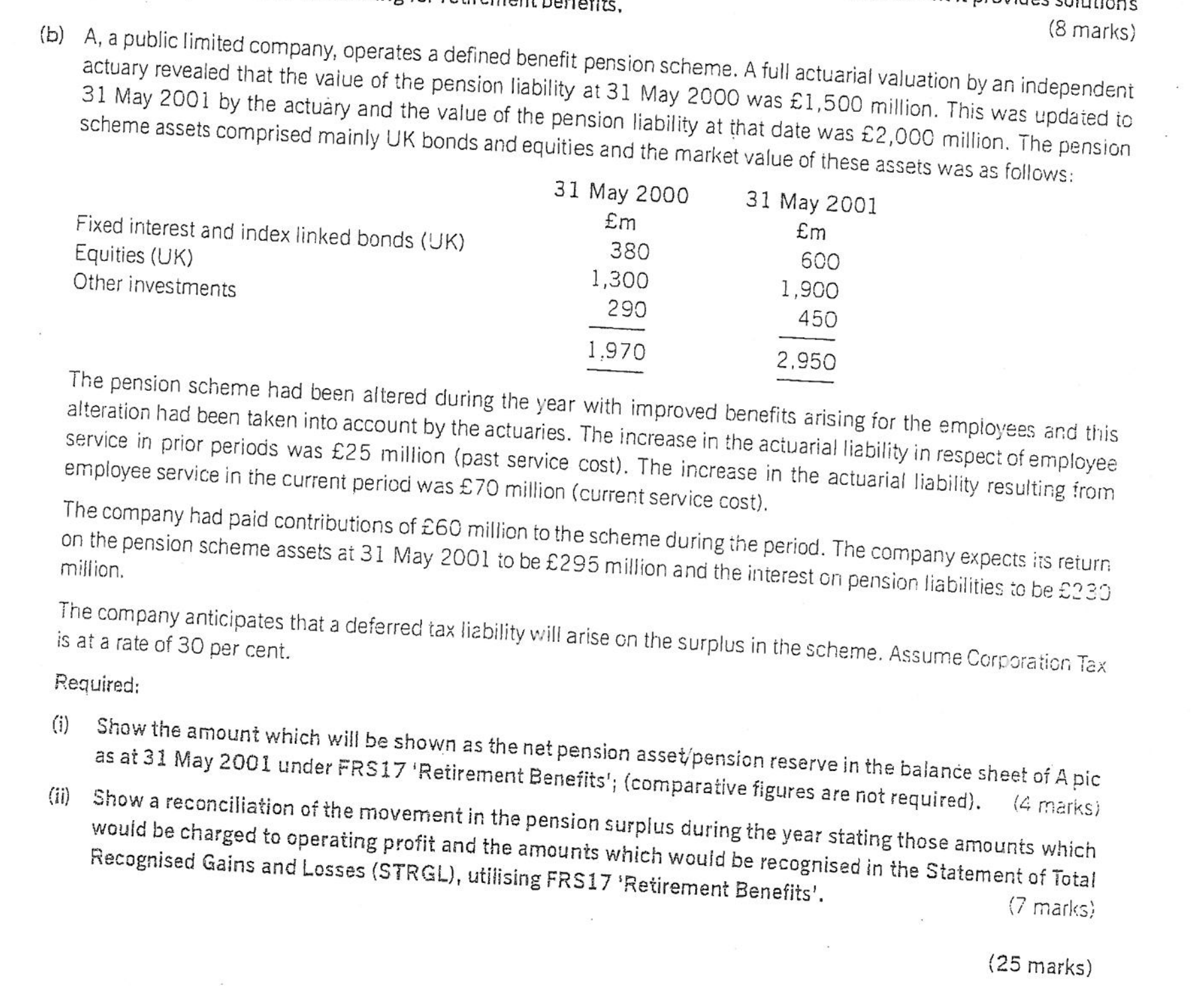

(b) A, a public limited company, operates a defined benefit pension scheme. A full actuarial valuation by an independent actuary revealed that the value of the pension liability at 31 May 2000 was £1,500 million. This was updated to 31 May 2001 by the actuary and the value of the pension liability at that date was £2,000 million. The pension scheme assets comprised mainly UK bonds and equities and the market value of these assets was as follows:

31 May 2000 31 May 2001 £m £m Fixed interest and index linked bonds (UK) 380 600 Equities (UK) 1,300 1,900 Other investments 290 450 1,970 2,950

The pension scheme had been altered during the year with improved benefits arising for the employees and this alteration had been taken into account by the actuaries. The increase in the actuarial liability in respect of employee service in prior periods was £25 million (past service cost). The increase in the actuarial liability resulting from employee service in the current period was £70 million (current service cost).

The company had paid contributions of £60 million to the scheme during the period. The company expects its return on the pension scheme assets at 31 May 2001 to be £295 million and the interest on pension liabilities to be £225 million.

The company anticipates that a deferred tax liability will arise on the surplus in the scheme. Assume Corporation Tax is at a rate of 30 per cent.

Required: (i) Show the amount which will be shown as the net pension asset/pension reserve in the balance sheet of A plc as at 31 May 2001 under FRS17 ‘Retirement Benefits’; (comparative figures are not required). (4 marks) (ii) Show a reconciliation of the movement in the pension surplus during the year stating those amounts which would be charged to operating profit and the amounts which would be recognised in the Statement of Total Recognised Gains and Losses (STRGL), utilising FRS17 ‘Retirement Benefits’. (7 marks)

(25 marks)

(b) A公司,一家公众有限公司,运营一个确定福利养老金计划benefit pension scheme。一位独立精算师进行的完整精算评估显示,截至2000年5月31日,养老金负债的价值为15亿英镑。该精算师在2001年5月31日更新了数据,养老金负债的价值为20亿英镑。养老金计划资产主要由英国债券和股票组成,这些资产的市场价值如下:

2000年5月31日 2001年5月31日 £m £m 固定利息和指数挂钩债券 (UK) 380 600 股票 (UK) 1,300 1,900 其他投资 290 450 总计 1,970 2,950

去年,养老金计划进行了变动,为员工带来了更好的福利,精算师已经考虑了这些变动。因员工在先前时期的服务所导致的精算负债增加了2500万英镑(过去服务成本)。因员工在当前时期的服务所导致的精算负债增加了7000万英镑(当前服务成本)。

公司在此期间向计划支付了6000万英镑的贡献。公司预计截至2001年5月31日的养老金计划资产回报为2.95亿英镑,对养老金负债的利息为2.25亿英镑。

公司预计,养老金计划中的盈余将产生递延所得税负债。假设公司税率为30%。

要求: (i) 根据FRS17《退休福利》,截至2001年5月31日A公司资产负债表中将显示的净养老金资产/养老金准备金金额是多少;(不需要对比数字)。(4分)

(ii) 展示一年内养老金盈余变动的调节,说明哪些金额将计入营业利润,以及在《总认可收益和损失表》(STRGL)中将确认哪些金额,使用FRS17《退休福利》进行说明。(7分)

(共25分)

请您稍等,我将先读取您上传的图片内容,然后用中文为您解答图片中的养老金计算会计题目。

根据图片中提供的信息,我们需要完成两项任务:

(i) 根据FRS17《退休福利》,截至2001年5月31日,A公司的资产负债表中会显示的净养老金资产/养老金准备金金额。 (ii) 对年内养老金盈余变动进行调节,并说明哪些金额会计入营运利润,哪些金额会在《总认可收益和损失表》(STRGL)中被确认,同时使用FRS17《退休福利》进行说明。

让我们用中文逐一解答。

(i) 2001年5月31日的净养老金资产/准备金金额计算如下:

- 养老金计划资产的市值 = 600m + 1,900m + 450m = £2,950m

- 养老金负债 = £2,000m

- 净养老金资产/准备金 = 养老金计划资产的市值 - 养老金负债 = £2,950m - £2,000m = £950m

所以,在资产负债表中将显示£950m作为净养老金资产/准备金。

(ii) 年内养老金盈余变动的调节如下:

- 期初养老金计划资产的市值 = £1,970m

- 期末养老金计划资产的市值 = £2,950m

- 养老金计划资产增加 = £2,950m - £1,970m = £980m

- 公司对计划资产的贡献 = £60m

- 公司期望的计划资产回报 = £295m

- 公司对养老金负债的利息成本 = £225m

- 过去服务成本 = £25m

- 当前服务成本 = £70m

- 养老金计划资产实际回报 = £2,950m - £1,970m - £60m = £920m

- 养老金盈余 = £920m - £295m - £225m - £25m - £70m = £305m

调节后的养老金盈余,将计入营运利润的部分有当前服务成本£70m和利息成本£225m。而在STRGL中将确认的部分包括过去服务成本£25m和计划资产的实际回报与预期回报之间的差异,即£920m - £295m = £625m。

需要注意的是,此计算不包括潜在的递延税项影响。假设公司税率为30%,那么基于£305m的养老金盈余,预计产生的递延税负债为£91.5m(即£305m * 30%)。这将在资产负债表中作为减项考虑。

| PENSION SCHEMES - EXAMPLE 1 | |||||||

| W1 | |||||||

| £m | |||||||

| Pension scheme assets at 31-5-01 | 2950 | ||||||

| Actuarial value of liability精算负债 | -2000 | ||||||

| Pension scheme surplus养老金计划盈余 | 950 | ||||||

| Deferred tax liability at 30% 递延税负债 | -285 | ||||||

| Net pension scheme asset at 31-5-01 | 665 | ||||||

| W2 | |||||||

| £m | |||||||

| Surplus in scheme at 1-6-00 (1970 - 1500) | 470 | ||||||

| Past service cost | -25 | ||||||

| Current service cost | -70 | ||||||

| Contributions into scheme | 60 | ||||||

| Expected return on assets | 295 | ||||||

| Interest on liabilities | -230 | ||||||

| Actuarial gain in the year精算盈利 | 450 | Bal fig | |||||

| Surplus in scheme at 31-5-01 (2950 - 2000) | 950 |

这个表格是一个典型的养老金计划的例子,展示了养老金计划的资产、负债以及盈余状况。下面我将解释每个项目的意义:

W1 - 养老金计划盈余及净资产

-

养老金计划资产于2001年5月31日(£m 2950): 这是指公司养老金计划中所有资产(如债券、股票、其他投资)的市场价值总和。

-

精算负债(-£m 2000): 公司需为未来养老金支付承担的现值负债,通常由精算师计算。

-

养老金计划盈余Pension scheme surplus(£m 950): 这是养老金计划资产减去精算负债后的余额,即盈余。

-

递延税负债按30%计Deferred tax liability at 30%(-£m 285): 基于养老金计划盈余,预计将产生的递延税负债。计算方法是盈余金额乘以税率。 = 950 x 30 %

-

截至2001年5月31日的净养老金计划资产(£m 665): 扣除预计的递延税负债后,养老金计划的净资产值。

W2 - 养老金计划盈余变动

-

2000年6月1日计划中的盈余(1970 - 1500 = £m 470): 上一年度末养老金计划的盈余,计算为养老金计划资产减去精算负债。

-

过去服务成本(-£m 25): 因过去增加的养老金福利导致精算负债增加的成本。

-

当前服务成本(-£m 70): 当年度员工服务对应的养老金成本。

-

向计划的投入(£m 60): 公司在当年度向养老金计划中支付的资金。

-

资产预期回报(£m 295): 预计养老金计划资产在年度中的投资回报。

-

负债利息(-£m 230): 养老金计划负债在年度中产生的利息成本。

-

年内精算盈利(£m 450,余额数字): 指因市场价值变动等因素,养老金计划资产实际价值超出预期计算值的部分。

-

2001年5月31日计划中的盈余(2950 - 2000 = £m 950): 年末养老金计划的盈余,计算为养老金计划资产减去精算负债。

这些计算反映了一年内养老金计划的财务变动,是会计和财务报告中重要的部分,用于决定公司在养老金计划方面的财务状况。

| BALANCE SHEET AT 31 MAY 2001 | |||

| (STATEMENT OF FINANCIAL POSITION) | |||

| £m | |||

| Net Pension Scheme Asset (W1)净养老金计划资产 | 665 | ||

| PROFIT AND LOSS ACCOUNT FOR YEAR ENDED 31 MAY 2001 | |||

| (INCOME STATEMENT) | |||

| £m | |||

| Administrative expenses W2 | 95 | (25 + 70) | |

| Interest receivable W2 | 65 | (295 - 230) | |

| STATEMENT OF TOTAL RECOGNISED GAINS AND LOSSES总认可收益和损失表 | |||

| (STATEMENT OF TOTAL COMPREHENSIVE INCOME)总综合收益表) | |||

| £m | |||

| Actuarial gain(W2)精算盈利 | 450 |

以下是表格的中文翻译:

截至2001年5月31日的资产负债表

(财务状况表)

金额(百万英镑)

净养老金计划资产 (W1) 665

截至2001年5月31日的损益表

(收入表)

金额(百万英镑)

管理费用 (W2) 95 (25 + 70)

利息收入 (W2) 65 (295 - 230)

总认可收益和损失表

(总综合收益表)

金额(百万英镑)

精算盈利 (W2) 450

在这个表格中,“W1”和“W2”是工作底稿的标记,分别代表不同的计算和分析过程。这些工作底稿通常包含了详细的计算步骤,以支持表格中给出的最终数字。

这个表格是关于截至2001年5月31日的资产负债表(财务状况表)、损益表(收入表)以及总认可收益和损失表(总综合收益表)的一部分。下面我将详细解释表格的每一项:

资产负债表截至2001年5月31日

- 净养老金计划资产 (W1) - £m 665: 这是公司资产负债表上显示的金额,代表公司养老金计划的净资产。这是根据工作底稿W1计算出的,养老金计划资产减去负债和递延税后的余额。

损益表截至2001年5月31日

-

管理费用 (W2) - £m 95 (25 + 70): 这一部分反映了公司损益表中的管理费用,包括了过去服务成本£25m和当前服务成本£70m。这些是公司在本财务年度内,根据工作底稿W2,需认为养老金计划所承担的成本。

-

利息收入 (W2) - £m 65 (295 - 230): 这表示公司在财务年度内从养老金计划资产中获得的预期回报(£295m),减去对养老金负债的利息成本(£230m),得到的净利息收入。

总认可收益和损失表

- 精算盈利 (W2) - £m 450: 这项反映了公司在财务年度内,养老金计划资产的市场价值相比精算预期有所增加,实现的精算盈利。这不计入损益表,而是直接计入股东权益,体现在总认可收益和损失表中。

现在,让我们返回图片中的问题来进行解读。图片中的问题要求我们:

(i) 根据FRS17《退休福利》,展示截至2001年5月31日的A公司资产负债表中将显示的净养老金资产/养老金准备金金额。

(ii) 展示一年内养老金盈余变动的调节,并说明哪些金额会计入营业利润,哪些金额会在总认可收益和损失表中被确认,使用FRS17《退休福利》进行说明。

基于上面的表格解释:

(i) 净养老金计划资产是£665m,这将在资产负债表中显示。

(ii) 损益表将显示作为管理费用的£95m(包括过去服务成本和当前服务成本)和作为利息收入的£65m。而总认可收益和损失表将显示精算盈利£450m。这些项目分别体现了养老金计划在财务报告中的不同方面,按照FRS17的要求进行了适当处理。

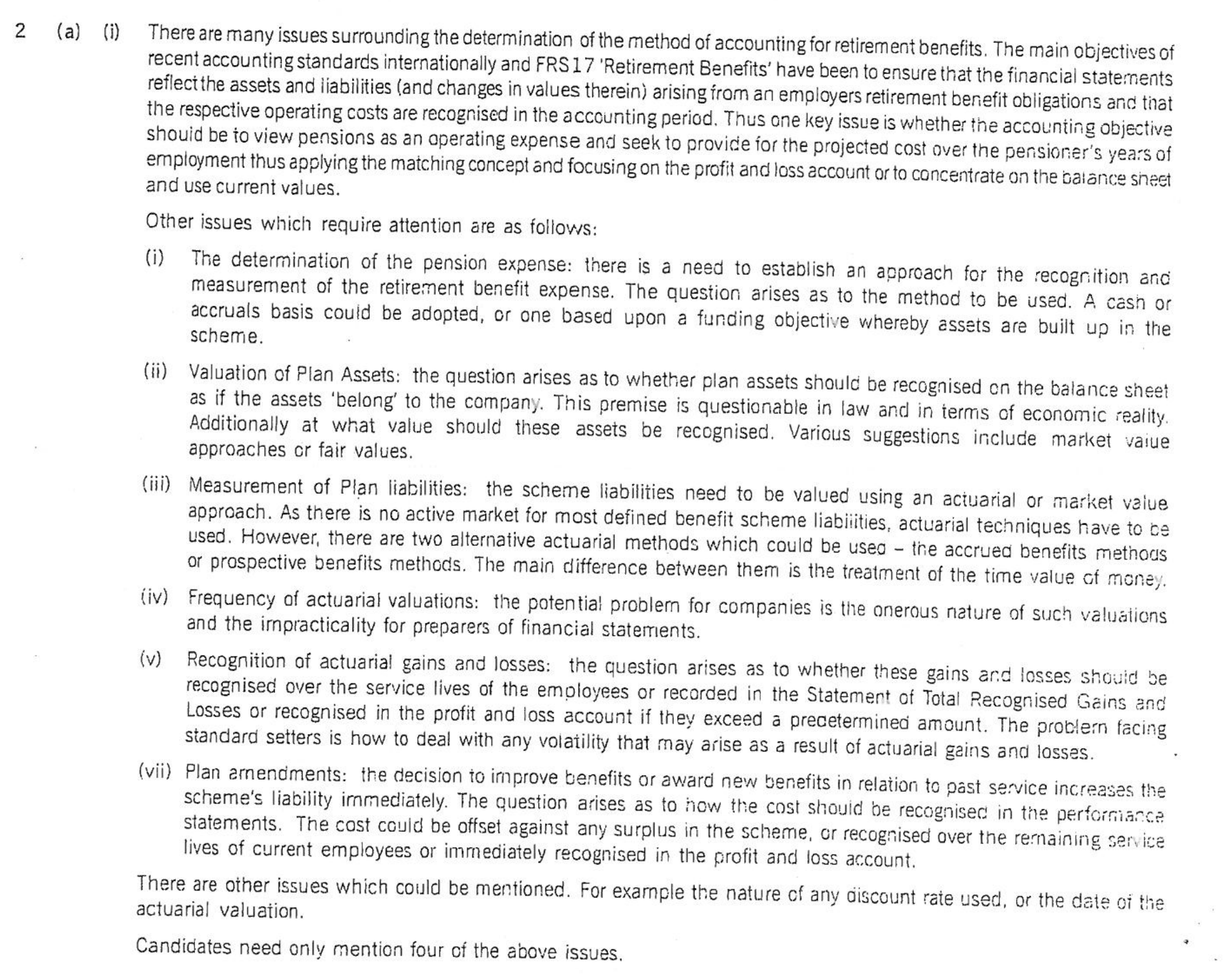

(a) (i)There are many issues surrounding the determination of the method of accounting for retirement benefits, The main objectives ofrecent accounting standarcds internationally and FRS 17 "Retirement Benefits' have been to ensure that the financial statemnentsreflecthe assets and liabilities (and changes in values therein) arising from an employers retirement benefit obligations and thatthe respective operating costs are recognised in the accounting period, Thus one key issue is whether the accounting objectiveshouid be to view pensions as an operating expense and seek to provide for the projected cost over the pensioner's years ofemployment thus applying the matching concept and focusing on the profit and loss account or to concentrate on the caiance sneeand uVari?usrent values Other issues which require attention are as follows:

(1)The determination of the pension expense确定养老金费用: there is a need to establish an apprcach for the recognition anddmand measurementhe retirement benefit expense. The question arises as to the method to be used. A cash oraccruals basis could be adopted, or one based upon a funding objective whereby assets are built up in thescheme

(2)Valuation of Plan Assets计划资产的评估: the question arises as to whether plan assets should be recoerecognised he balance sheetas if the assets "belong to the company. This premise is questionable in law and in terms of economic realityAdditionally at what value should these assets be recognised. Varius suggestions include market value approaches or fair values.

3.Measurement of Plan liabilities计划负债的衡量: the scheme liabilities need to be valued using an actuarial or market vaiue(iapproach. As there is no active market for most defined benefit scheme liabilities, actuarial techniques have to ceused. However, there are two alternative actuarial methods which could be used - the accrued benefits methogsor prospective benefits methods. The main difference between them is the treatment of the time value cf money

4)Freauency of actuarial valuations精算评估的频率: the potentia problern for companies is the onerous nature of such valuaticnsand the impracticality for preparers of financial statements.

5) Recognition of actuarial gains and losses精算收益和损失的确认: the auestion arises as to whether these gains and osses shouid berecognised oyer the service lives of the emoloyees or recorded in the Statement of Total Recognised Gains anoLosses or recognised in the profit and loss account if they exceed a precetermined amount. The problern facingstandard setters is how to deal with any volatility that may arise as a result cf actuarial gains and losses

(6)Plan amendments计划修正: the decision to improve benefits or award new benefits in relation to past service increases thescheme's liability immediately. The question arises as to how the cost shouid be recognised in the perforniancastatements. The cost could be offset against any surplus in the scheme, or recognised over the remaining servicelives of current employees or immnediately recognised in the profit and loss accountThere are other issues which could be mentioned. For example the nature cf any discount rate used, or the date oi theactuarial valuation. Candidates need only mention four of the above issues

(a) (i) 确定退休福利会计处理方法的问题有很多。国际上最近的会计准则和FRS 17《退休福利》的主要目标是确保财务报表反映了雇主退休福利义务产生的资产和负债(及其价值变化),并且相应的运营成本在会计期间被确认。因此,一个关键问题是会计目标是否应该将养老金视为经营费用,并寻求提供养老金成本的预测,从而应用匹配概念并关注损益表,或者集中在资产负债表上使用当前值。

需要关注的其他问题包括:

- 1.确定养老金费用determination of the pension expense:需要建立一个方法来认定和衡量退休福利费用。问题是应使用何种方法。可以采用现金或权责发生制,或者基于资金目标,通过计划在计划中积累资产。

- 2.计划资产的评估Valuation of Plan Assets:问题是计划资产是否应该在资产负债表上确认,就好像这些资产“属于公司”。这一前提在法律和经济实际中是有疑问的。此外,这些资产应以何种价值被确认。不同的建议包括市场价值方法或公平价值。

- 3.计划负债的衡量:计划负债需要使用精算或市场价值方法来评估。由于大多数确定福利计划负债没有活跃市场,因此必须使用精算技术。然而,有两种替代的精算方法可以使用 - 累积福利方法或预期福利方法。它们之间的主要区别是处理货币时间价值。

- 精算评估的频率:公司潜在的问题是这种评估的繁重性质以及财务报表编制者的不切实际。

- 5.精算收益和损失的确认:问题是这些收益和损失应该在员工的服务年限内被确认,还是记录在总认可收益和损失表中,或者在超过预定金额时在损益表中确认。标准制定者面临的问题是如何处理由于精算收益和损失可能产生的任何波动。

- 6.计划修正:改善福利或授予与过去服务相关的新福利的决定立即增加计划的负债。问题是性能报表中应如何确认成本。成本可以抵消计划中的任何盈余,或者在现有员工的剩余服务年限内确认,或者立即在损益表中确认。还有其他问题可以提及。例如使用的任何贴现率的性质,或精算评估的日期。 候选人只需提及以上四个问题中的任何四个。

FRS 17是什么的缩写

ChatGPT

ChatGPT

FRS 17是英国财务报告准则17(UK Financial Reporting Standard 17)的缩写,它涉及退休福利的处理。FRS 17引入了一个重要要求,即在赞助雇主的资产负债表中确认和披露养老基金赤字和盈余的完整金额。该准则适用于2014年12月31日或之前开始的报告期。自2015年1月1日起,员工福利的报告由FRS 102的第28节覆盖。